Article Text

Abstract

While health policy scholars wish to encourage the creation of technologies that bring more value to healthcare, they may not fully understand the mandate of venture capitalists and how they operate. This paper aims to clarify how venture capital operates and to illustrate its influence over the kinds of technologies that make their way into healthcare systems. The paper draws on the international innovation policy scholarship and the lessons our research team learned throughout a 5-year fieldwork conducted in Quebec (Canada). Current policies support the development of technologies that capital investors identify as valuable, and which may not align with important health needs. The level of congruence between a given health technology-based venture and the mandate of venture capital is highly variable, explaining why some types of innovation may never come into existence. While venture capitalists’ mandate and worldview are extraneous to healthcare, they shape health technologies in several, tangible ways. Clinical leaders and health policy scholars could play a more active role in innovation policy. Because certain types of technology are more likely than others to help tackle the intractable problems of healthcare systems, public policies should be equipped to promote those that address the needs of a growing elderly population, support patients who are afflicted by chronic diseases and reduce health disparities.

- Economics

- Accessible

- Affordable

This is an Open Access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/

Statistics from Altmetric.com

Venture capital and new medical technologies

As industrialised countries develop strategies to expedite the commercial translation of biomedical discoveries1 and bring technological innovations closer to the clinic, policy initiatives that give a greater role to venture capital warrant careful examination.2 Such policies may include fiscal incentives to attract venture capital as well as the creation of funds dedicated to help health technology-based ventures grow.3–5

Drawing on the international innovation policy scholarship and a programme of research that examined the evolution of five Canadian health technology-based ventures over an 11-year period, this paper clarifies how venture capital operates and influences the kinds of technologies that make their way into healthcare systems. Our research entailed extensive document analyses (ie, annual reports, press releases, media coverage) and in-depth interviews with technology developers, capital investors, regulators and policymakers. This qualitative data set enabled our team to examine, from a health policy standpoint, the impact of business models, capital investment and economic policy on technology design processes.

In this paper, our aim is to provide health services and policy researchers with the key lessons that pertain more specifically to the way current policy arrangements in systems of innovation support the development of technologies that capital investors identify as valuable, and which may not align with important health needs. While health services and policy scholars wish to encourage the creation of technologies that bring more value to healthcare, they rarely fully understand the mandate of venture capitalists and how they operate. A better understanding of how this form of financing ultimately affects healthcare systems would help health services and policy scholars play a more active role in innovation policy.

Policy expectations towards venture capital

In the past decades, North American and European countries actively sought to increase the size of their venture capital markets.6–10 The levels of venture capital available to Canadian life sciences companies have more than doubled from 2001 to 2010.11 In Europe, the UK enjoyed in 2009 the second largest venture capital market, accounting for 21% of all investments. In the same year, 20% of the UK £677 million of venture capital was invested in the health sector.4

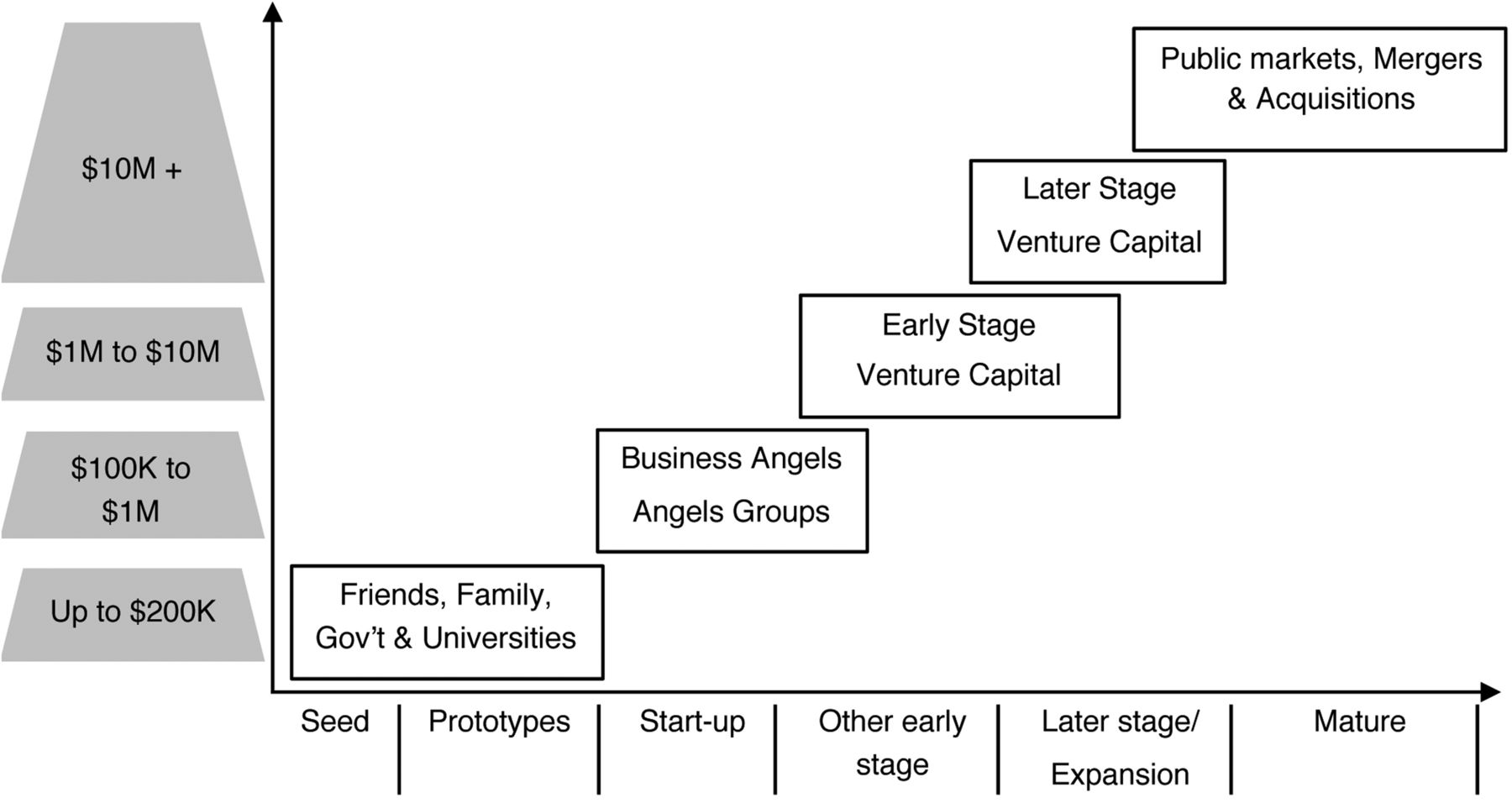

Examining panel data of 17 European Union countries, Faria and Barbosa6 found that venture capitalists are “more willing to support innovation only after the initial and more uncertain stage of technology development has been overcome.” This tendency partly explains why the Horizon 2020 Programme protected up to €320.14 million in 2014 to help innovative firms to gain access to various types of risk financing.5 To foster the growth of technology-based ventures, venture capital typically steps in after entrepreneurs have fleshed out their core innovative idea with the financial support of governments, relatives and ‘angels’ (eg, wealthy individuals who finance entrepreneurial activities).3 As figure 1 indicates, venture capital provides both early-stage and late-stage financing, which precedes more substantive sources of capital such as public markets.

Funding chain by stage of development and size of investment in $C (adapted from ref. 4).

The innovation policy scholarship posits that venture capital-backed ventures are likely to outperform non-venture capital-backed ventures.6–8 The main arguments are that ‘investors can identify firms with hidden value’, that their investments operate as a ‘signal of the quality of the ventures for uninformed third parties’, and that they bring ‘external resources and competencies that would be out of reach’ without their endorsement.7 Informed by such literature, policymakers rely on ‘two pillars’ to foster the venture capital market. First, they seek to increase the ‘demand’ for venture capital by providing ‘generous subsidies’ and fiscal advantages to entrepreneurs so as to augment ‘birth rate’ of innovative firms.7 Second, they seek to increase the ‘supply’ of venture capital through ‘co-investment schemes, the launch of new government-owned venture capital companies and favourable tax treatment of capital gains’.7 Along those lines, the UK government created many funds since 2000, including the High Technology Fund, the Early Growth Funds and the Enterprise Capital Funds. Such funds played a particularly important role in early-stage financing in the following years, witnessing a peak in 2008 during which 68% of all early-stage venture capital investments were publicly backed.4

How venture capital operates

The two-pillar innovation strategy implies that public resources, either through taxation or ‘hands-off’ financing, are put to the service of venture capital, whose mandate largely conditions how capital-backed technology development processes unfold. Venture capitalists commit financial resources for a specified period of time to small privately held companies with few tangible assets and that rarely generate revenues alongside their initial research and development activities. What makes venture capital risky is the ‘illiquid’ nature of the investment during this period, meaning that the resources invested cannot be easily withdrawn.8 ,12 ,13 The window of opportunity for a ‘liquidity event’ such as acquisition by another company or an initial public offering—which provides the ability to sell shares to the public—is generally within 5 years.11 These so-called ‘exit’ events enable venture capitalists to recoup their investments and generate a return. Venture capital is very costly capital and the overarching principle is to generate the highest returns possible while knowing that most ventures fail.10 Song et al9 found that only 36% of American ventures created between 1991 and 2000 had survived after 4 years and this rate fell to 21.9% after 5 years. The returns from a subset of firms have to be much greater than average to make up for the expected failures, and yield above 20% returns for the investment portfolio as a whole.8 ,11 For instance, the top 25th centile of capital-backed UK firms generated returns ranging from 50% to 78% between 2003 and 2009, while the bottom 10 generated returns ranging from −14% to 0%.4

To successfully fulfil their mandate, venture capitalists generally seek to both pick winners and build them (see box 1).14 This means that they do not simply carefully choose entrepreneurs, but they also engage in ‘value-adding activities’.15 These activities include ‘coaching’ the ventures by providing the marketing and strategy support these young firms usually lack, professionalising their management by supporting the recruitment of seasoned managers, and facilitating alliances with key third parties within the industry. By having a seat at the Board of Directors of the fledgling firm, capital investors occupy an influential position from which they shape its governance (ie, advisory committees, nomination of high-level executives, partnerships) and seek to align technology developers towards their own vision.10 ,13 All of these value-adding activities are geared at augmenting the value of the investment, a process that entails shaping both the firm and the technology being developed.16 ,17

What venture capitalists do to fulfil their mandate

Picking likely winners and ‘de-risking’ deals at the outset

Helping grow the ventures and intervening when progress is lacking

Maintaining a dominant position until the liquidity event (eg, holding a seat at the Board of Directors of the ventures, enforcing a timeframe for instalments)

Pushing capital-backed ventures to reach key milestones swiftly to avoid additional financing and the dilution of shares this implies

Negotiating contracts and providing compensation for those who facilitate timely exit

Venture capitalists exert control over technology design processes by setting the ‘term sheet’, which defines the milestones (eg, clinical trials, regulatory approval, sales) at which money is made available.13 This has direct implications for technology design priorities. Among the early-stage health technology companies we studied, for example, one clinically led firm had to modify the key goal of its labour monitoring system, which was to reduce unnecessary caesarean sections, and instead develop medicolegal functionalities for physician insurers who were more likely to purchase the system.18 This redesign of the system enabled their business to expedite sales and generate revenues.

As table 1 indicates, the level of congruence between a venture that seeks to bring to the clinic a new technology and the mandate of venture capital varies. The heart ablation catheter venture deployed an international cadre of clinical investigators that generated the evidence required for regulatory approval in different countries and, by offering to investors credible prospect of rapid and continued expansion, it was able to secure several rounds of capital investments. By developing a revenue-generating technology for medical specialists, this venture replicated a business model that is well established in the biomedical sector. Among the three examples, it is the home monitoring system venture where the level of congruence between the mandate of venture capital and the innovation was the lowest. Such a technology creates value for hospitals that do not generate revenues out of hospitalisations and have incentives to prevent deterioration of chronically ill patients, such as Health Maintenance Organizations(HMOs) in the USA or publicly funded integrated healthcare systems in Canada or the UK.

Contrasting examples of the level of congruence between the mandate of venture capital and health technology-based ventures (adapted from ref. 18)

Among the ventures that are developing an innovation to support the provision of clinical services, those that are seen as more congruent with the goal of venture capital and less risky possess similar characteristics; their innovations address very large and reachable markets, enable physicians to generate revenues, and will ultimately be acquired by an established medical device manufacturer (for an exit to take place).18

The mandate of venture capitalists may, in principle, prove compatible with supporting ventures that address important health needs. But this is likely to happen by accident, not by design. Survey findings indicate that up to 85% of capital investors consider ‘not at all or somewhat important’ public health impact.19 Investors also contend that regulatory requirements decrease the ‘chance that an investment will be made in a ‘new area’’ and increase the chance an investment will be ‘made in a ‘me-too’ space’ (eg, where a slightly different technology is already implemented and marketed).19 To strike lucrative ‘homeruns’ within a predefined period of time, venture capitalists seek indeed to ‘de-risk’ the deal at the outset by enforcing stringent agreements.18

By and large, venture capitalists affect the kinds of technologies available to patients, clinicians and healthcare systems by investing in certain ventures and not in others, managing their growth and controlling the progression of their innovative products (see box 2).

How venture capital influences the technologies available to physicians, patients and healthcare systems

Venture capitalists choose the sectors and innovations that are worth investing in, and increase chances of success

Within the timeframe on which Returns on Investment (ROI) are estimated at the outset, the progression of capital-backed ventures is steered towards the most profitable exit

Technology design priorities are influenced by the time and resource constraints that venture capitalists enforce

The centrality of venture capital in innovation systems

While venture capital is not designed to fulfil ‘society's most urgent public health priorities’,20 it occupies a central position in what innovation policy scholars define as ‘innovation systems’.21 Figure 2 illustrates the relationships between key milestones in the health technology development pathway and the institutions that define the ‘rules of the game’, that is, the specific requirements that players have to fulfil.22 The rules set by these institutions have both constraining and enabling effects. For instance, regulatory agencies exert control over the safety of medical devices, but by enabling market access, they also provide economic worth to technology-based ventures (as reflected in the value of their share).18

{kind=link}

{kind=link}

Institutions that enable and constrain the emergence, development and commercialisation of health technology.

While institutional rules are often described as hindrances by investors and technology developers, such rules contribute to the stability and functioning of innovation systems: they provide incentives for innovation, supply information, reduce uncertainty, foster cooperation and make available mechanisms to handle conflicts.21 Without such rules, venture capitalists and technology developers would simply be unable to cooperate, trust each other, succeed in developing and commercialising a new medical technology, and persuade physicians and patients that their technologies are trustworthy. Overall, and as underscored by figure 2, it is innovation policy, venture capital, financial markets, and legal and corporate governance frameworks that deeply structure upstream innovation processes.16 ,17 ,22–24 Long before health policy comes into play, the way venture capital interlocks with these institutions has lasting downstream consequences for healthcare systems.

One key lesson for clinical leaders and health services and policy scholars is that, despite the fact that public policies increasingly encourage venture capital-backed technological innovation in health, handling the subtleties associated with the fulfilment of valuable healthcare goals is neither part of venture capitalists’ mandate, nor of their worldview. Examining recent data from the USA, Fleming20 observed two types of shift in venture capital investments. There has been a shift away from life sciences to other sectors, such as early-stage internet and consumer-oriented start-ups, and a shift within the life sciences from early-stage to later-stage investments. The first shift is conditioned by the standpoint from which the value of the firms is assessed—that of an investment portfolio—which remains largely indifferent to the societal value of the innovation such firms may generate.24 The second shift underscores that the overarching goal of venture capital is not so much to foster the creation of innovation, but to extract economic value from innovative firms and technologies.2 ,6 ,16

Bringing health policy considerations into innovation policy

For Robinson,25 the current emphasis on more sophisticated and cost-conscious purchasing in healthcare may have the ‘potential to increase the social value of innovation’ by focusing technology developers on ‘the preferences and pocketbooks’ of their customers. Beyond their cost, we believe the value of innovations will increase only if clinical leaders and health services and policy experts contribute much more actively than they have done so far to innovation policy. Policy efforts in the past decades have been devoted to the consolidation of Health Technology Assessment (HTA) and evidence-based decision-making.26 This is not sufficient: institutional arrangements that currently prevail in systems of innovation push public policies to support the development of those technologies capital investors identify as valuable. Capital-backed technology development operates according to rules that are foreign to the fulfilment of healthcare needs, and the consideration of healthcare system-level challenges.27

The policy assumption on which governments, capital investors and technology developers currently operate is that publicly funded research should translate into private entrepreneurial activities because technological innovation contributes to a nation's economic growth.1 ,2 ,28 This economic orientation in public policy establishes favourable conditions for venture capitalists to play an influential role in systems of innovation and shape key decisions about health needs.18 Nevertheless, if the key policy goal is to increase the relevance of innovations from a health policy standpoint, it is the knowledge and insights of health experts that should be foregrounded. Their expertise could shape the processes and criteria on which key bodies allocate important resources to health innovation, and where articulating more clearly a ‘demand’ for technologies that are valuable from a health system perspective matters (see box 3).

Decision-making bodies where the expertise of clinical leaders and health services and policy scholars could contribute to shape health innovation

Research funding agencies where specific programmes dedicated to research and development in health are designed

Research centres of university teaching hospitals where the principles and goals of collaborative research between clinical innovators and industry are established

Health technology priority setting and procurement committees where the value of new technologies is defined, sending ‘signals’ to entrepreneurs

Currently, the financial speculative rules at play too easily reconcile policy goals that are distinct—health and wealth—‘without asking first what healthcare needs and challenges should be addressed’.29 Because certain types of technology are more likely than others to help tackle the ‘intractable problems’30 of healthcare systems, public policies should be equipped to promote those that address the needs of a growing elderly population, support patients who are afflicted by chronic diseases and reduce health disparities. Such knowledge can only come from clinical leaders and health services and policy scholars.

References

Footnotes

Contributors PL drafted the preliminary versions of the paper. Both FAM and GD contributed substantially to its design, and to the analysis and interpretation of existing evidence. PL, FAM and GD were all engaged in a programme of research on the evolution of five Canadian technology-based ventures over an 11-year period. All authors approved the final version of the paper and are accountable for it. PL is the guarantor.

Funding This research was funded by an operating grant from the Canadian Institutes of Health Research (CIHR; #MOP-89 776). PL holds the Canada Research Chair on Health Innovations (2010–2015).

Competing interests None declared.

Ethics approval The Ethics Review Board of the University of Montreal approved the study.

Provenance and peer review Not commissioned; externally peer reviewed.